April 20 (Lagos) - The 2014 oil price crash decimated Nigeria’s oil earnings, the country’s primary source of dollar inflows, exerting depreciation and liquidity pressure on the local currency.

In response to the external shock, the Central Bank of Nigeria (CBN) allowed the Naira to depreciate by 11% in the last quarter of 2014. But despite persistent pressure on the exchange rate, the CBN opted to defend the currency by burning through its external reserves and enacting measures to manage dollar demand in the economy.

This approach accelerated capital flight from the economy as investors feared a forced devaluation, further drying up dollar liquidity and adversely affecting dollar-dependent sectors of the economy.

By the end of 2015, 18 months after the oil price slide began, the Naira had lost 18% of its value against the dollar, while the Kazakhstan Tenge and Angola Kwanza shed 46% and 28% of their dollar worth, showing how tightly the CBN had held the currency.

A revival in Niger Delta militancy in early 2016 hammered the final nail in Nigeria’s oil production coffin, weakening the CBN’s position even as Nigeria’s economy headed towards its first recession in 25 years.

The CBN took action by floating the naira in June 2016, before effectively reneging on the move as the exchange rate depreciated more than expected and the official exchange rate averaged as high as NGN316/USD in August 2016.

Fearing the short-term economic and political impact of the currency debasement, the CBN resumed its tight grip on the foreign exchange (FX) market, which only served to hit the economy more – Nigeria recorded its first full-year recession in 25 years, and inflation hit a decade-high.

The peak of the currency crisis came in February 2017 when the dollar broke the ?500 level in the black market (official rate at the time: NGN305/USD), but soon turned amid a simultaneous rise in domestic oil production and improving global oil prices.

The CBN began to boost dollar liquidity through a series of regular currency auctions, before enacting the “Investors’ & Exporters’” (I&E) currency window or “NAFEX” fixing, a segment of the FX market where the naira could freely float.

The NAFEX fixing has proved to be a game-changer in the FX story, and almost a year to the date of its conception (21st April 2017), we explore the most significant differences it has made to the Nigerian economy.

From famine to feast in the FX market

The NAFEX fixing has been a boon to Nigeria’s FX market, boosting liquidity and price discovery, but also fostering investor confidence in the economy. The improvement in the FX market has been a critical element of Nigeria’s economic recovery.

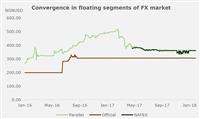

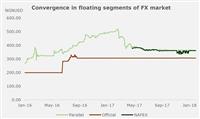

After an average 52% spread between the official and parallel market rates in 2016, and a peak spread of 70% in February 2017, the introduction of the NAFEX fixing triggered a convergence in rates. The improvement in market liquidity and transparency drove the parallel market rate from its peak of NGN520/USD in February 2017 to NGN390/USD by the end of April 2017.

Promisingly, although the naira continues to be priced at a discount in floating segments compared to its official levels, we have observed a sustained near-parity between the NAFEX and parallel market rates, providing more clarity on the market price of the Naira and reducing arbitrage in the economy.

Average monthly foreign exchange turnover recorded by FMDQ stood at $12 billion, USD 7 billion, and, USD10 billion for 2015, 2016, and 2017 respectively. Furthermore, H2’17 average was USD 13 billion, compared to USD 7 billion in H1’17, indicating the impact the NAFEX window has had on boosting dollar liquidity. Estimates of autonomous inflows into the “I&E” window are imprecise, but conservative guidance is at least $10 billion since inception, a far cry from Nigeria’s capital flight experience of 2014-2016.

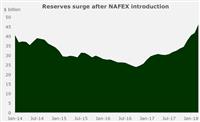

The improvement in the FX picture can also be seen in the evolution of Nigeria’s external reserves. External reserves almost doubled from its trough of $24 billion in October 2016 to $46 billion in March 2018. A significant portion of this increase can be attributed to Federal Government external borrowing (c.$7.3 billion), currency swaps with commercial banks, and higher oil earnings, but also reflects higher autonomous dollar inflows into the economy.

Crucially, the rise in reserves shows that the CBN is in a stronger position to defend the Naira and maintain its stability in floating segments of the market, thus reducing the depreciation risk attached to the currency in the near term.

NAFEX ignites equity market party

The most obvious effect of the NAFEX fixing has been on the Nigerian Stock Exchange (NSE). Given the high historical correlation between global oil prices and activity in Nigeria’s equity market, the oil price crash spelt trouble for the NSE, driving negative market performance and lower trading activity in the 2014-2016 period.

The introduction of the NAFEX fixing encouraged foreign investors to return to the space, spurring a market rally that earned the

NSE a podium finish on the global equity markets league table in 2017.

The

NSE All-Share Index lost 40% of its value between its 2014-peak in July and the end of April 2017. Yet, in the three months following the NAFEX fixing, the market had gained 39%. By the end of the year, the index had surged 42%.

Foreign investors have always played an outsized role in the Nigerian equity market, not just in their direct investments, but in their ability to steer market sentiment. Therefore, capital flight depressed market turnover, with domestic investors lacking the risk appetite to place big bets in the market.

The NAFEX fixing changed everything, attracting sizable foreign flows to the market once again, which in turn encouraged greater domestic investor participation in the market. As a comparison, average daily market turnover on the

NSE for 2015, 2016, and 2017 reads as follows: N 3.7 billion, N 2.2 billion, and N 3.6 billion.

What next for the foreign exchange market?

According to analysts at Vetiva Capital Management Ltd in Victoria Island, The Nigerian economy is already benefiting from the NAFEX fixing through improved dollar liquidity and investor confidence, with the dark days of currency crisis looking like distant history.

Should Nigeria be re-included in the J.P. Morgan Emerging Market Bond Index, it would provide another boost and almost bring us full circle to a pre-currency crisis period. On the FX market, the CBN seems keen on persisting with the current multiple exchange rate structure, though there is a slight possibility that it would collapse the different markets into its official window, should it feel it has the ammunition to stabilize a floating Naira at that level.

Longer-term, the exchange rate remains vulnerable to oil shocks, and given the volatility of the global oil market and explosiveness of Niger Delta militant groups, Nigeria’s FX market is unlikely to attain the desired invulnerability anytime soon. For now, at least, we can raise a toast to the NAFEX window for the changes it has wrought.

reporting for easykobo.com on Friday, April 20 2018 from Lagos, Nigeria

Source - analysts at Vetiva Capital Management Ltd in Victoria Island